• 3 min read

ETH futures open interest climbs as spot buyers take charge

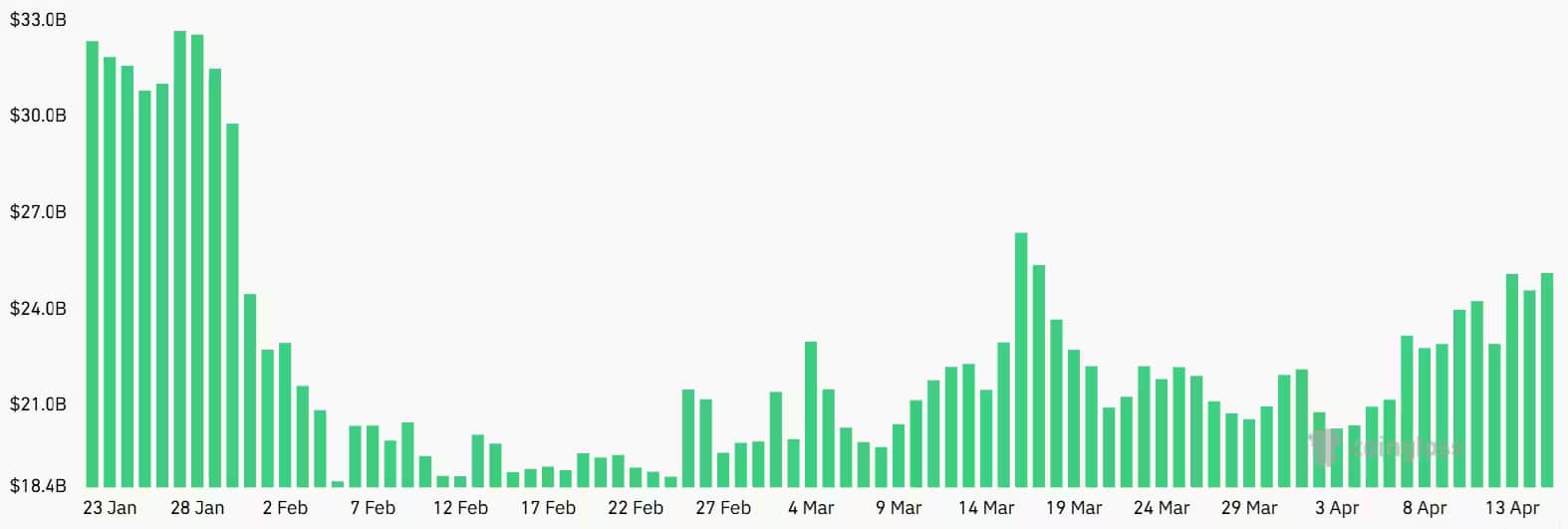

Ether’s latest bounce above $2,300 is doing something the market has not managed for 10 weeks: dragging ETH futures open interest higher without convincing traders to fully buy the rally. Open interest in ETH futures has

Image: cointelegraph.com

Ether’s latest bounce above $2,300 is doing something the market has not managed for 10 weeks: dragging ETH futures open interest higher without convincing traders to fully buy the rally. Open interest in ETH futures has climbed to $25.4 billion, but funding rates still look hesitant, which is a polite way of saying leveraged bulls are not exactly throwing confetti.

The split matters. Spot demand has been doing the heavy lifting, while derivatives traders seem content to watch from the sidelines – or even lean the other way. That kind of setup can support a rally for a while, but it also leaves ETH exposed if the buyers chasing actual coins stop showing up.

Spot inflows are doing the heavy lifting

US-listed Ether spot ETFs pulled in $248 million over the past 10 days, and that is the cleanest sign that capital is returning through the front door rather than the leverage hatch. Bitmine Immersion also said it bought $312 million worth of ETH, lifting its holdings to 4.87 million ETH, or $11.46 billion. The catch: those holdings are trading 13% below acquisition cost, so even the big believers are already sitting on paper losses.

Recommended reading

Iraq Licenses Starlink for Affordable Satellite Internet

ETH funding rates still don’t trust the move

ETH perpetual futures funding has failed to hold above 5% since Friday and has dipped below 0% more than once, which points to weak conviction among leveraged traders. In a healthy, balanced market, that rate usually sits somewhere between 5% and 10% to offset the cost of capital. Instead, the setup suggests a market that is still skeptical even as price has steadied above $2,300 and away from the $1,940 lows seen on March 29.

That caution is not irrational. Ether still has not reclaimed $2,400, even as the S&P 500 printed a new all-time high on Wednesday, a reminder that crypto is once again underperforming its own hype cycle while risk assets elsewhere keep partying.

Ethereum activity remains the weak spot

The bigger problem is not price. It is usage. Ethereum weekly DApps revenue has fallen to $11 million from $24 million in early February, and that slump has fed a familiar argument: if onchain activity is soft, the burn mechanic investors love to cite does less work, and ETH looks more like a macro trade than a productive network bet.

Competition is also getting sharper. Specialized blockchains such as Hyperliquid and Plasma are pulling some of the attention that once flowed automatically to Ethereum, while segments like memecoin launchpads, lending, exchanges, bridges, and collectibles have all been hit hard by the 2026 bear market. The few bright spots – prediction markets and real-world assets – have not been enough to reverse the slide in network revenue.

What traders will watch next

For now, ETH has the look of a spot-led recovery with nervous derivatives support. If institutional inflows keep coming and open interest keeps rising without a funding-rate blowoff, bulls get time to build a base. If not, the market may decide that $2,300 is less a launchpad than a waiting room.

Culture Editor

Maya explores gaming, streaming, and the internet as a place where people actually live. From deep-dives into creator economies to the anthropology of digital communities, she tracks platform drama and cultural shifts so you don't have to. She believes the best tech stories are fundamentally about human behavior.