OLED monitor shipments are still a niche business compared with LCD, but the pace of growth is hard to ignore. In the first quarter of 2026, global shipments fell 11% from the previous quarter and jumped 78% from a year earlier, according to TrendForce. The quarter-on-quarter dip looks like a hangover from a very strong fourth quarter of 2025; the bigger story is that more QD-OLED panels are getting out the door, and the market is starting to sort its winners.

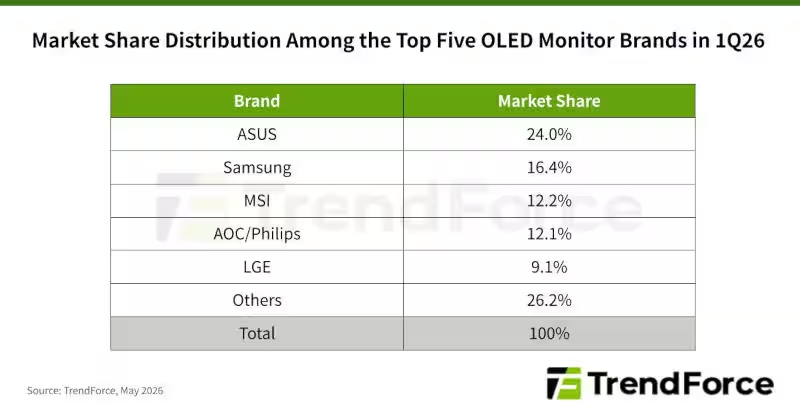

Asus finished first with a 24% share, helped by a broad lineup that included a 34-inch 360 Hz monitor and a portable 16-inch model. That kind of spread matters in a category where buyers are still deciding whether they want a gaming panel, a creator display, or something they can actually carry around without calling a chiropractor.

Samsung, MSI and AOC/Philips close behind

Samsung took second place with 16.4%, with its own QD-OLED panel production giving it a built-in advantage. TrendForce pointed to a 27-inch QHD model as one of the products behind that result. The vertical integration here is the obvious competitive edge: if you make the panels and the monitors, you are not waiting politely in someone else’s supply queue.

MSI ranked third at 12.2%, just ahead of AOC/Philips at 12.1%. MSI leaned on 31.5-inch models and expanded in both commercial and gaming displays, including a 27-inch UHD monitor and a 34-inch gaming display with a 360 Hz refresh rate. AOC/Philips went after the entry-level OLED crowd with 27-inch QHD models, and that was enough to keep it right in the hunt for third place.

LG Electronics is leaning on ultrawide OLED monitors

LG Electronics was fifth with 9.1%, but it has a different playbook: the company launched an exclusive 39-inch WUHD model at 165 Hz, and TrendForce expects that display to add meaningfully to shipments in the second quarter as well. In the first quarter, ultrawide models accounted for 40% of LG’s OLED monitor shipments, and that share could climb to about 45% in the current quarter.

That mix suggests the OLED monitor market is still rewarding aggressive product segmentation rather than a single ”best” spec sheet. For now, Asus has the broadest reach, Samsung has the panel advantage, and everyone else is fighting for position in a category that is growing fast enough to make even an 11% quarterly dip look like noise.