If you’ve held off upgrading your PC because DDR5 kits looked absurdly expensive, Europe may be where you start looking again. After a steep spike that pushed average 32 GB kits into the mid‑hundreds, recent price data shows a modest but meaningful pullback – not a return to bargain basement levels, but a correction that matters for anyone shopping right now.

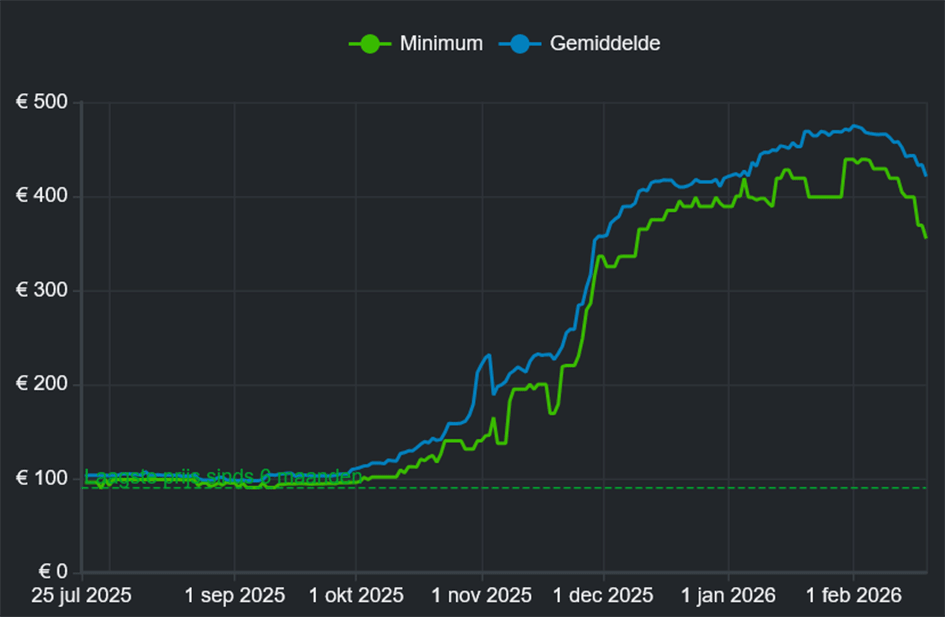

The signal came from enthusiasts: a pricing chart shared on a popular PC community tracked the average price of a 32 GB DDR5 kit across the EU from late July 2025 to February 2026. The chart shows average prices creeping around €95-€100 through early autumn, then a sharp climb starting in October and peaking in early February at roughly €430-€470 on average (with minimum prices slightly lower). Toward the end of the tracked period both average and minimum lines trend downward.

That community chart grabbed attention because it put numbers on a problem a lot of buyers felt: DDR5 costs went from comfortably affordable to shockingly high in a few months. Independent retail trackers that monitor listings on Amazon Germany confirm the same pattern: several well‑known 32 GB DDR5-6000/6400 kits have fallen back from their February peaks. For example, Corsair’s Vengeance RGB 32 GB DDR5-6000 slipped from around €480 in early February to about €425 at the time of tracking; Kingston’s Fury Beast 32 GB DDR5-6000 moved from roughly €550 in early January to €463. Other kits are similarly below their recent highs.

Two important clarifications: European retail prices normally include VAT (value added tax), so headline comparisons with U.S. sticker prices aren’t apples to apples; and while the U.S. market showed smaller corrections for some kits, it hasn’t broadly matched the European downtick.

Why prices exploded – and why they’re easing

The spike and the partial retreat are symptoms of three forces colliding. First, supply constraints. DRAM production faced bottlenecks through late 2025 as makers wrestled with yields on newer process nodes and prioritized higher‑margin server/industrial demand. Second, demand dynamics. Renewed interest in high‑performance platforms and continued growth in data‑center memory needs pushed inventories thin. Third, retail behavior: when stock is low and demand visible, retailers inflate margins until competition or buyers force cuts.

The easing looks partly mechanical. High retail prices suppressed demand enough that some retailers began cutting tags to get inventory moving. Longer term, full normalization depends on supply catching up – which the industry itself expects only as new DRAM production capacity comes online in late 2026-2027 and as process transitions improve yields and output.

Who wins and who loses

Memory manufacturers were the short‑term winners while prices were high: higher average selling prices boosted revenue without an immediate jump in manufacturing cost. Retailers also profited where they could, but they’re the first to suffer when demand collapses and markdowns are necessary. Gamers and builders are the losers – they postponed purchases or paid premiums. Now that prices are easing, buyers gain negotiating power, but chipmakers will still control the timing of a full recovery back to reasonable pricing.

Why this isn’t a full reversal – yet

A modest correction doesn’t mean DDR5 is back to the prices you saw in 2023. There are structural reasons prices can stay elevated for a while: limited near‑term capacity additions, the continuing pivot of some production toward higher‑margin server DRAM and HBM, and the simple fact that manufacturers can throttle supply to sustain ASPs. Expect volatility: prices will bounce as inventory ebbs and flows, seasonal demand shifts, and new fabs ramp.

For shoppers: if you need memory now, the recent pullback makes a purchase less painful than it was in February. If you can wait, the best chance of a deeper drop comes once new DRAM capacity actually starts producing at scale – probably not until late 2026 or 2027. Watch trackers and retailer stock rather than headlines: discounts and bundle deals will be the practical sign that the market has moved.

The takeaway

The recent movement in Europe is welcome: it proves that the market responds when prices rise too far. But this is a correction, not a reset. Real relief depends on more supply, better yields, or a meaningful drop in demand. In the meantime, buyers have workarounds – shop smart, compare VAT‑inclusive prices, and be ready to pounce on genuine discounts.