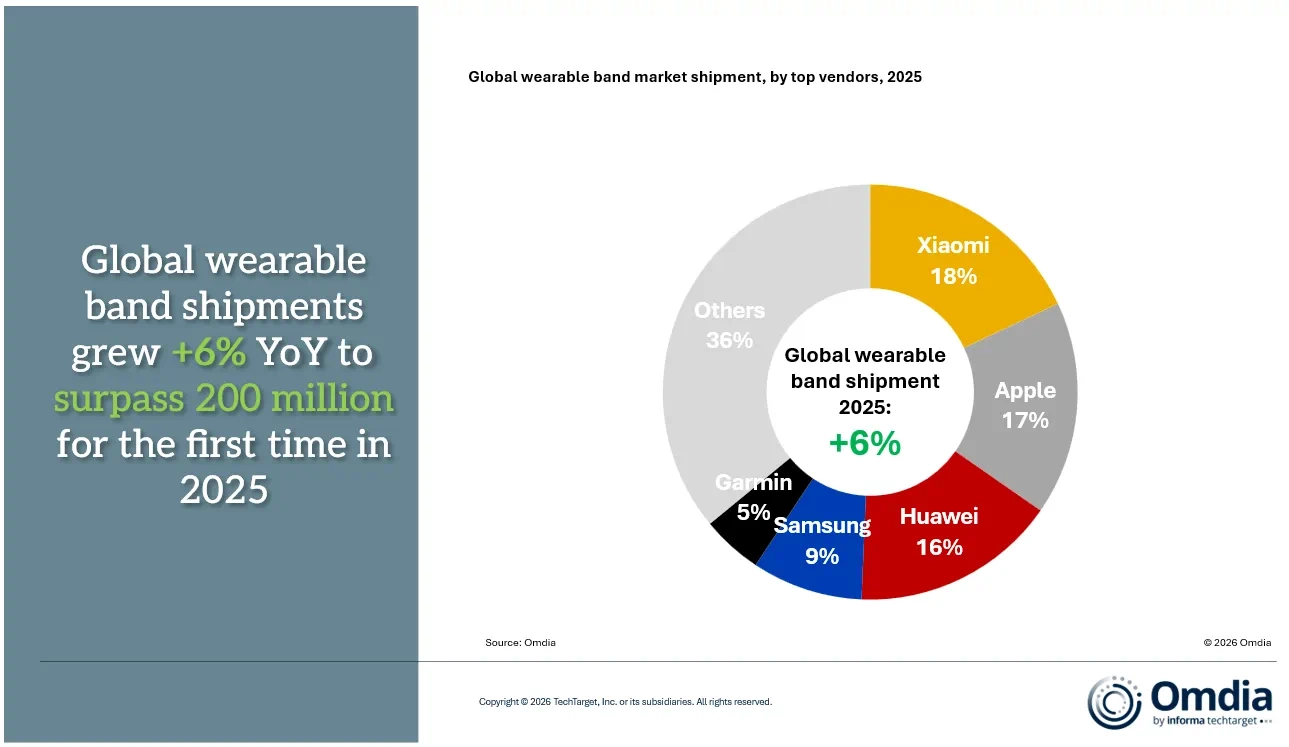

The global wearables market is suddenly too tight to breathe. Shipments passed 200 million units in 2025, up 6% year over year, and Xiaomi reclaimed the No. 1 spot after five years out of the lead – but only by a whisker.

Omdia’s numbers show Xiaomi with 18% of worldwide wearable shipments, Apple at 17%, and Huawei at 16%. Samsung and Garmin follow, with 9% and 5%, respectively. Those single-digit gaps make this less a clear victory than a photo finish: less than a percentage point separates the top three.

What actually changed

This isn’t a story about one moonshot product. Xiaomi’s strength is breadth: the Mi Band family moves massive volumes in the ultra‑affordable segment, while inexpensive smartwatches nudge up average selling prices without straying into premium margins. In short, Xiaomi wins on scale and price elasticity – the sort of economics that look pedestrian in headlines but devastatingly effective on balance sheets.

Meanwhile, Apple still dominates premium wearables. Its advantage isn’t cheap hardware; it’s that the Apple Watch ties deeply into the iPhone, health services, and an ecosystem many users are already locked into. Huawei has likewise played a territorial game – strong in China with a wide portfolio and a push toward sports and health features – while Samsung and Garmin continue to own niche and mid‑premium pockets of the market.

Why ecosystem beats specs now

Hardware differences are flattening. Step counters, heart rate sensors, and decent battery life are table stakes across the board. The new battleground is the invisible glue: how well a wearable talks to phones, smart home kits, cars, and subscription services. That ”stickiness” turns a cheap band into a retention tool for a wider platform.

That shift favors companies with sprawling product portfolios and services to sell. Xiaomi’s ”Human × Car × Home” approach, which ties appliances, phones, and cars into one ecosystem, amplifies the value of a low‑cost band in ways pure hardware players can’t easily match.

Who wins and who should worry

Winners: Xiaomi gets a headline and momentum without relying on pricier margins; Chinese brands that combine low‑cost hardware with broad IoT platforms look well positioned; and companies that can monetize through services (health subscriptions, device tie‑ins) will extract more lifetime value.

At risk: Pure hardware plays that can’t convert device buyers into long‑term platform users. Premium brands like Apple aren’t losing – they remain dominant in the high end – but they must keep justifying their price premium with health features and services. Smaller western challengers that once hoped to scale by selling increasingly better sensors will find the economics tough unless they pivot to ecosystems or unique software.

What’s missing from the applause

Two blind spots remain. First, quality of data and long‑term software support: cheap devices sell fast, but users notice stale apps and disappearing update schedules. Second, services and privacy. As wearables collect more continuous health signals, the companies that monetize those streams will face fresh scrutiny over data access and regulatory risk – a potential headache if the market tilts toward subscription models.

How this race will likely play out in 2026

The rankings are fragile. With Xiaomi, Apple, and Huawei separated by slivers of market share, a single product cycle, pricing push, or stronger regional performance could shuffle the table again. Expect the next moves to be less about radical new sensors and more about bundling – discounted wearables with phones, fitness services, car tie‑ins – and experiments in subscription revenue.

For consumers, that’s mostly good: cheaper devices with better cross‑device conveniences. For investors and competitors, it raises a more interesting question: who can turn low‑margin hardware into durable, recurring income without losing customers to rivals that simply undercut on price?

Numbers to remember: 200 million wearables shipped in 2025 (+6%); Xiaomi 18%, Apple 17%, Huawei 16%, Samsung 9%, Garmin 5%. Those decimals now carry market fortunes.