Public companies that treat bitcoin as the treasury are living inside a contradiction: the asset’s headline volatility makes for dramatic accounting losses, while the market rewards narrative and conviction more than granular disclosure. That tension is what’s behind the latest dustup around Metaplanet – and why the company’s insistence it was ”transparent” answers one question but ignores another.

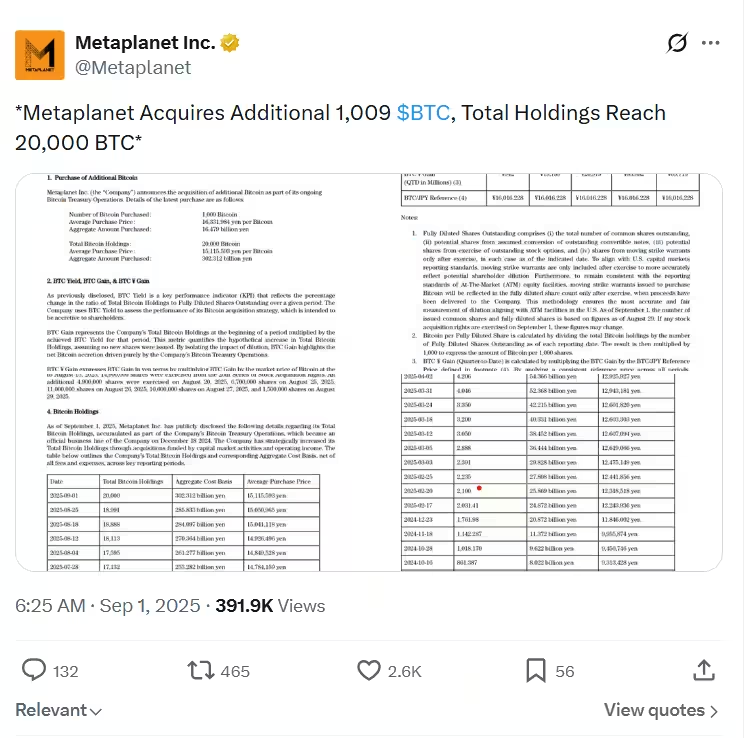

Last week Metaplanet’s CEO pushed back against online accusations that the firm hid price‑sensitive Bitcoin activity and downplayed risks. The company’s real‑time dashboard shows four purchases in September 2025 – 1,009 BTC on Sept. 1, 136 BTC on Sept. 8, 5,419 BTC on Sept. 22 and 5,268 BTC on Sept. 30 – and its filings report a fiscal 2025 revenue of 8.9 billion Japanese yen and a net loss of about $680 million tied to the drop in its bitcoin holdings. Metaplanet also disclosed a credit facility opened in October 2025 and draws in November and December, while saying the lender asked that its identity and exact rates remain private.

Those are public facts. The question investors and regulators will now press on is not whether the trades were announced after they happened, but whether the disclosures are sufficient to judge the balance between opportunistic accumulation, derivatives exposure and leverage.

A familiar playbook with familiar blind spots

Metaplanet’s approach – buy bitcoin, sell puts and put spreads to acquire coins below spot and generate options income, and use secured borrowing against BTC – is recognizable. Other listed bitcoin treasury plays have used the same toolkit and suffered the same painful accounting headlines when prices fell. Public filings can show revenue from options and lending income, yet also reveal massive non‑cash impairment or mark‑to‑market losses on the asset base.

That mismatch explains why managements highlight operating metrics and cash flows while critics point to headline losses. Both views are technically true. What’s missing from most corporate defenses, though, is a full mapping of downside scenarios: counterparty concentrations, collateral triggers, margin mechanics and the tail risk embedded in aggressive options selling during a volatile market.

Why ”we announced it” isn’t the same as usable disclosure

Announcing a purchase or publishing aggregate holdings is basic transparency. It becomes less useful if the accounting treatment and off‑balance‑sheet mechanics allow a company to tout rising revenue from options while paper losses on held bitcoin swamp equity. Investors trying to value a bitcoin treasury company need the timing and pricing of large option positions, the strike profile of sold puts, and the precise terms of any secured borrowings – not just the fact that a facility exists.

There’s also a practical issue: counterparties sometimes insist on confidentiality. That is common in finance, but in a business model where the underlying collateral is highly volatile, broad confidentiality reduces the usefulness of a disclosure. Saying ”the counterparty requested anonymity” explains why a line item is redacted, but doesn’t help a shareholder assess counterparty credit risk or liquidation thresholds.

Context from the field

This is not hypothetical. Other public holders have reported eye‑watering impairments during drawdowns, underlining how quickly a treasury story can flip to an accounting problem. Past failures in the crypto ecosystem – from highly leveraged trading firms to centralized lenders that collapsed under market stress – show the same pattern: opacity + leverage + volatile collateral = outsized losses for creditors and equity.

Options selling can smooth returns in calm markets but amplifies risk in stressed ones. Selling puts or put spreads can lead to large coin allocations at worse prices than expected or to concentrated short positions if hedges fail. That trade-off is central to the debate: are these strategies conservative accumulation tools, or asymmetric bets that will blow up in a severe downturn?

What investors should ask next

If you own or watch companies running a bitcoin treasury, press for the details that matter in stress scenarios:

– A schedule of option expiries and strikes, with notional exposure broken out by maturity bucket.

– Collateral haircuts, liquidation thresholds and cure mechanics for any bitcoin‑backed borrowing.

– Concentration and identity of counterparties where possible, and whether counterparties impose restrictions on the company’s disclosure.

Verdict and outlook

Metaplanet’s insistence that it reported purchases and borrowing is defensible. But ”we said it” is only the first step toward meaningful transparency. The real debate is whether the corporate treasury model for an inherently volatile asset should demand a higher bar of disclosure and stronger guardrails around leverage and derivatives. Expect analysts to dig deeper, auditors to get stricter, and investors to demand scenario‑level reporting – or to vote with their feet if answers are vague.

Companies that can answer the uncomfortable questions – not just recite the press releases – will be treated differently by markets. Those that skirt them will remain a headline risk waiting for the next price shock.

Image: Metaplanet announcement of BTC purchase